Labuan Income Tax Rate

Income from intellectual property assets held by a Labuan entity is subjected to the prevailing rate under the Income Tax Act 1967 of 24. Individuals Individual residents in Labuan with income accruing in or derived from Malaysia are subject to tax.

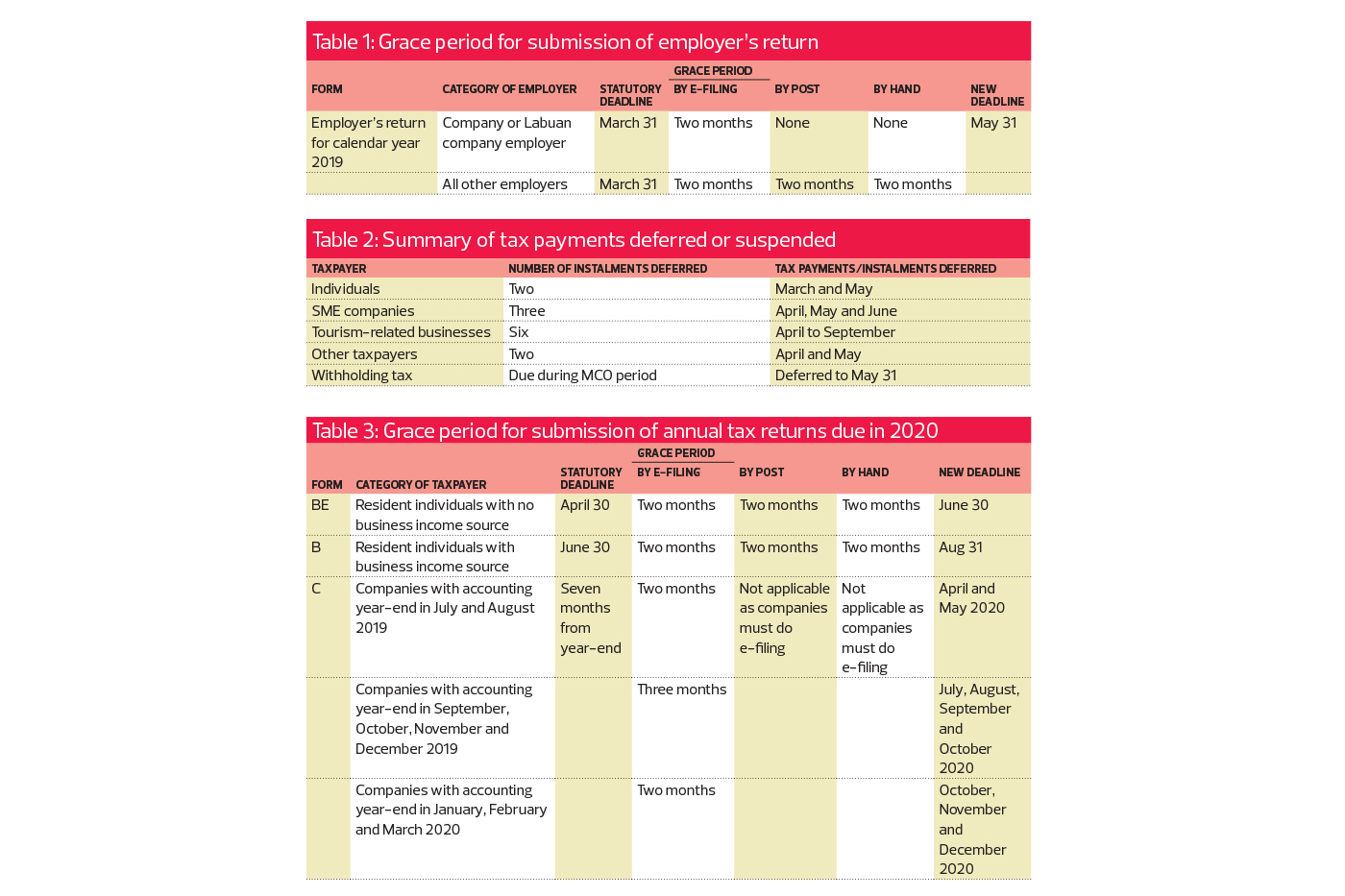

Taxplanning Tax Measures Announced During The Mco The Edge Markets

Under the amendment to Section 4 4 of the LBATA income derived from royalty or intellectual property rights is now subject to tax under the Malaysian Income Tax Act 1967 ITA rather than under the LBATA.

Labuan income tax rate. Income from intellectual property rights is subject to tax therefore the rate is 24. Any income incurred from intellectual property rights is now subject to tax under the Malaysian Income Tax Act 1967 ITA instead of the LBATA. Other Malaysian non-Labuan entities deriving income from Malaysia are subject to tax under the ITA where the usual rate of tax applicable to companies is currently 25.

Under the amendment to Section 4 4 of the LBATA income gained from royalty or intellectual property rights is now subject to tax under the Malaysian Income Tax Act 1967 ITA instead under the LBATA. The prevailing income tax rate for companies non-SMEs in Malaysia under the ITA is 24. Labuan Taxes are Easy Labuan holding company is subject to 0 tax zero tax Labuan licensed company is subject to 3 tax Malaysia Double Taxation Agreement DTA protects your income from being taxed twice.

Labuan company that have opted to be taxed under the Malaysia Onshore Income Tax Act 1967 will follow the local corporate tax rate of 17 on the first RM 600000 followed by 24 on subsequent chargeable income. However it has been proposed that the rate be reduced to 24 from the year of assessment 2016. This means that companies that engage in non-trading activities such as holdign companies are not subject to the tax at all.

The new tax law also tackles the CRS common reporting system by OECD requirement of commercial substance for tax proofing by introducing the needs of staffs and minimum spending particularly for license entities and some special entities were introduced. Tax rate The tax rate applicable to a Labuan entity is 3 on the chargeable income from Labuan trading activities only. Prior to the changes Malaysian taxpayers could claim a 100 percent tax deduction on payments made to a Labuan entity.

Business entities can no longer claim full tax deductions for payments made to a Labuan legal entity they only have the option to claim partial deductions according to the type of payment for example 67 for lease rentals and interest payments and 3 for other types of payments. The main tax advantages for investors who choose to open a company in Labuan include a low 3 tax rate applicable to income derived from trading activities. Corporate tax was cut from 28 to 27 in 2007 to 26 in 2008 and to 25 in 2009.

Is it possible to open a bank account for Labuan Company in Labuan. Resident status of a Labuan entity. Foreign sourced income received in Malaysia by resident individuals are tax-exempt.

Do I need to inform Labuan Financial Services Authority when I register a Labuan company. This means the income from the Labuan non-trading activities ie the holding of investments in securities stocks shares loans deposits or other properties of a Labuan entity is not subject to tax at all. That said it goes without saying that there are stringent requirements to be complied with prior to the enjoyment of the special tax rate.

The healdine rate of corporate tax in Malaysia is 25 2013. This means the new prevailing tax rate is 24 percent. Resident companies in Labuan are subjected to a Corporate Income Tax rate of 3 on annual audited taxable net income under Labuans Tax Regulations.

A competitive tax regime Labuan business activities as defined in the Labuan Business Activity Tax 1990 LBATA 1990 which provides. Malaysian Sdn Bhd Company pays a tax rate as follows. The tax rate is 19 and for every additional RM 1 the rate is 24.

What are the minimum director and shareholder requirements for a Labuan company. A non-resident company also pays 25 2013 on chargeable income. Resident Status of a Labuan Entity.

Companies carrying a non-trading activities is not charged tax ie. As a company incorporated under the Labuan Companies Act 1990 it is generally only required to pay taxes at a rate of 3 as compared to the standard rate of 24 for a typical Sdn Bhd. This means that all Labuan entities that carry on a Labuan trading activity and comply with the relevant economic substance requirements shall be subject to tax at the rate of 3 on its chargeable profits.

Taxation of 3 of net audited profits or a flat rate of MYR20000 to be elected yearly if the company is undertaking trading activities. The general income tax rate for organisations non-SMEs in Malaysia under the ITA is 24. The rate of tax ranges from 0 to 28 for resident individuals and a flat rate of 28 for non-resident individuals.

Do Labuan Company need to file annual return. Must financial statements of Labuan.

Mysst

0 comments: